In the nine months ended December, Rallis India launched six new products. Of these, four have got a good response, the management told analysts. The firm intends to launch one more product in Q4 and add at least two new products every year.

Going ahead, the March quarter outlook is decent—new products and a better rabi season should help maintain its revenue momentum. With raw material prices easing, there is further scope for margin improvement.

“Both our industry checks and management commentary suggest the easing of raw material prices from Q3 and this should flow through in gross margins from Q4FY20," analysts at Investec Capital Services (India) Pvt. Ltd said in a note.

Having said that, easing raw material prices have resulted in pricing pressure on certain products in both India and the international market. While subdued demand in the US (export business) is a headwind, the bigger challenge for investors is revenue growth visibility.

High reservoir levels and healthy soil moisture content are propelling the rabi season. But how much of this positive momentum will be carried into kharif 2020 remains to be seen. Further, a good rabi harvest supported by favourable prices is crucial to sustain farm sentiments.

With the Rallis India stock’s valuations now at 17 times FY21 earnings estimates, some analysts, however, advise caution. “Given limited earnings visibility, we would not argue for a further re-rating. We would remain on the sidelines for now, awaiting better visibility into the seasonally more important kharif season," said an analyst with a domestic broking firm, on condition of anonymity.

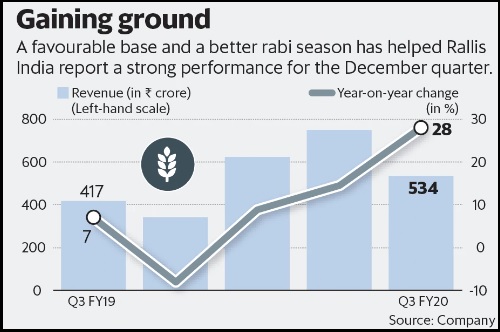

Agrochemicals maker Rallis India Ltd gained 20% in the last three trading sessions, adding ₹798 crore to its market capitalization. The Street was impressed with its December quarter show, which prompted an earnings upgrade.

Revenue increased by 28%. Operating earnings doubled. The firm benefited from the sales spillover of the delayed kharif (summer) and better rabi (winter) crop season.

Renewed sales push helped. The new management stepped up dealer additions, product launches and realigned the credit policy with the industry. This lifted the revenue in India by 35%.

In the nine months ended December, Rallis India launched six new products. Of these, four have got a good response, the management told analysts. The firm intends to launch one more product in Q4 and add at least two new products every year.

Going ahead, the March quarter outlook is decent—new products and a better rabi season should help maintain its revenue momentum. With raw material prices easing, there is further scope for margin improvement.

“Both our industry checks and management commentary suggest the easing of raw material prices from Q3 and this should flow through in gross margins from Q4FY20," analysts at Investec Capital Services (India) Pvt. Ltd said in a note.

Having said that, easing raw material prices have resulted in pricing pressure on certain products in both India and the international market. While subdued demand in the US (export business) is a headwind, the bigger challenge for investors is revenue growth visibility.

High reservoir levels and healthy soil moisture content are propelling the rabi season. But how much of this positive momentum will be carried into kharif 2020 remains to be seen. Further, a good rabi harvest supported by favourable prices is crucial to sustain farm sentiments.

With the Rallis India stock’s valuations now at 17 times FY21 earnings estimates, some analysts, however, advise caution. “Given limited earnings visibility, we would not argue for a further re-rating. We would remain on the sidelines for now, awaiting better visibility into the seasonally more important kharif season," said an analyst with a domestic broking firm, on condition of anonymity.

0 thoughts on “Rallis Indias strategy rejig pays off all eyes now on kharif 2020”