It has increased its branch network even as the lender is investing in its digital offerings. Chief executive officer Amitabh Chaudhry reiterated that both physical and digital are part of the plan to grow the balance sheet and acquire customers.

To be sure, the thrust on retail franchise is showing results as deposits are growing faster. Retail loans, of course, are galloping. The 25% retail loan expansion drove the total loan book growth to 18% for the December quarter. Loans to companies grew by 16% from a year ago period.

Analysts had hoped that the lender would increase its market share and it seems to have achieved this. Even fee income growth was healthy, led by retail rather than corporate.

The core income strength validates the faith that analysts had when earnings estimates were increased for the bank in the previous quarters.

That the stock has outperformed broad market indicates that investors have taken note that Axis Bank’s balance sheet is mending as well.

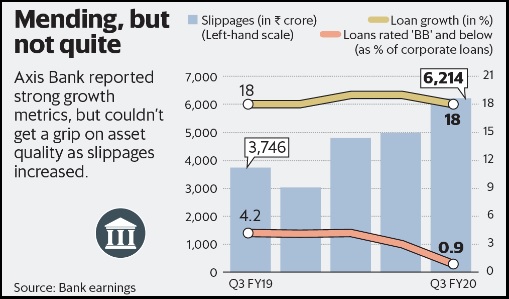

But this mending isn’t smooth.

Axis Bank saw its slippages unexpectedly rise for the December quarter. Corporate slippages are from known names, as the majority of them came from the bank’s watchlist of weak loans. But about 37% of total slippages came from outside this watchlist.

The share of non-corporate slippages has increased over time although on a net basis these are still a small percentage of the loan book.

The management has assured that slippages are under control and hopes to achieve a slippage ratio of 1% in the next few quarters.

For all its efforts, Axis Bank hasn’t been able to get a grip on its asset quality problem. To be fair, the bank cannot be blamed entirely. A slowing economy makes it difficult for companies to repay loans, putting pressure on asset quality for banks. Also, the lender had warned investors that slippages may remain elevated for some time.

Axis Bank also faced a hit of ₹1090 crore on its investment book due to default on interest payment on bonds by a housing finance company. Even as the bank fixes old problems, fresh troubles are brewing

It remains to be seen whether the strong operating performance would overshadow the bad loan worry.

" />

India’s banking history is awash with examples of how aggressive lending can lead to pain later. After all, lenders have been in the middle of such pain over the last four financial years.

Axis Bank is in the middle of another bout of aggressive lending, this time on the retail side. Would it pay off for the lender? For now, the aggression is surely giving it the love of investors.

The third largest private sector lender reported robust core income growth and exhibited that it is indeed growing into a strong retail bank.

It has increased its branch network even as the lender is investing in its digital offerings. Chief executive officer Amitabh Chaudhry reiterated that both physical and digital are part of the plan to grow the balance sheet and acquire customers.

To be sure, the thrust on retail franchise is showing results as deposits are growing faster. Retail loans, of course, are galloping. The 25% retail loan expansion drove the total loan book growth to 18% for the December quarter. Loans to companies grew by 16% from a year ago period.

Analysts had hoped that the lender would increase its market share and it seems to have achieved this. Even fee income growth was healthy, led by retail rather than corporate.

The core income strength validates the faith that analysts had when earnings estimates were increased for the bank in the previous quarters.

That the stock has outperformed broad market indicates that investors have taken note that Axis Bank’s balance sheet is mending as well.

But this mending isn’t smooth.

Axis Bank saw its slippages unexpectedly rise for the December quarter. Corporate slippages are from known names, as the majority of them came from the bank’s watchlist of weak loans. But about 37% of total slippages came from outside this watchlist.

The share of non-corporate slippages has increased over time although on a net basis these are still a small percentage of the loan book.

The management has assured that slippages are under control and hopes to achieve a slippage ratio of 1% in the next few quarters.

For all its efforts, Axis Bank hasn’t been able to get a grip on its asset quality problem. To be fair, the bank cannot be blamed entirely. A slowing economy makes it difficult for companies to repay loans, putting pressure on asset quality for banks. Also, the lender had warned investors that slippages may remain elevated for some time.

Axis Bank also faced a hit of ₹1090 crore on its investment book due to default on interest payment on bonds by a housing finance company. Even as the bank fixes old problems, fresh troubles are brewing

It remains to be seen whether the strong operating performance would overshadow the bad loan worry.

0 thoughts on “Axis Bank delivers on growth but trouble lingers on the bad loans front”