And if the sanguine view of HCL Tech’s product business prevails, investors may well witness a rerating. “It (the products business) contributed to overall Ebit margin in 3QFY20 and the trend could continue given the transition is still ongoing," JM Financial Institutional Securities Ltd said in a note. Ebit stands for earnings before interest and tax.

As pointed out earlier, not many are betting on that outcome, as the valuations suggest. HCL Tech’s shares trade at only around 12 times their one-year forward earnings estimates, far lower than market leader Tata Consultancy Services Ltd’s valuations of 20 times forward earnings.

" />

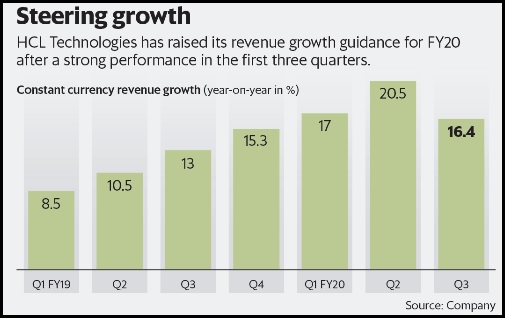

Shares of HCL Technologies Ltd fell 1.6% on Monday even though the company reported better-than-expected earnings for the December quarter. The 2.1% sequential revenue growth in constant currency terms, which exceeded the Street’s estimates and guidance for the full year, implies a healthy 2% sequential revenue growth in the March quarter as well.

So, what explains the negative reaction by investors? The main concern is that growth in Q3 was entirely driven by the products and platforms business segment, where performance tends to be lumpy. “We remain cautious on HCL’s significant products exposure," analysts at Jefferies India Pvt. Ltd wrote in a note to clients.

While the company’s acquisition-led strategy has helped bump up revenues, investors are concerned about the possibility of a decline in revenues and margins going forward, as the products are in so-called mature segments.

This concern is reflected in the firm’s valuations, which are nearly the same as Wipro Ltd, despite growing at a faster pace.

The IT, engineering and R&D services, which generated most of HCL Tech’s revenues, clocked a meagre 0.1-0.7% growth. Higher-than-expected furloughs and exit from certain low-margin, non-strategic engagements weighed on revenues of the traditional business last quarter.

Another concern is the outlook for FY21. “Outlook for FY21 growth may not be as rosy as in FY20 as HCL Tech has not booked any $1 billion type orders in FY20 unlike two in FY19," analysts at Nirmal Bang Institutional Equities said in a recent note.

Of course, there is also the general slowdown that is dragging down growth at all IT services firms.

The silver lining is that HCL Tech’s deal pipeline remains strong. The pace of contract renewals has been healthy and the pipeline has several large deals, according to the firm. So, order bookings can pick up in the current quarter, the management told analysts.

The proof of the pudding, of course, is in its eating. So, it will be critical for the company to report stronger growth in the core business in the coming quarters.

And if the sanguine view of HCL Tech’s product business prevails, investors may well witness a rerating. “It (the products business) contributed to overall Ebit margin in 3QFY20 and the trend could continue given the transition is still ongoing," JM Financial Institutional Securities Ltd said in a note. Ebit stands for earnings before interest and tax.

As pointed out earlier, not many are betting on that outcome, as the valuations suggest. HCL Tech’s shares trade at only around 12 times their one-year forward earnings estimates, far lower than market leader Tata Consultancy Services Ltd’s valuations of 20 times forward earnings.

0 thoughts on “Product led expansion turning off HCL Technologies shareholders”